Contact The Editor

Contact The Editor

Articles By This Author

Articles By This Author

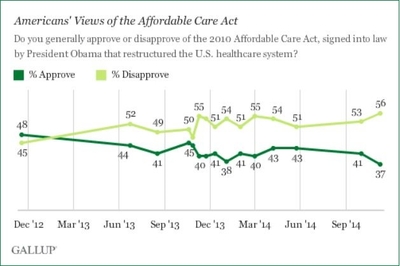

The second open enrollment period for health insurance under the Affordable Care Act is underway, and the law is more unpopular than ever. According to Gallup, a record-high 56 percent of Americans now disapprove of the 2010 law.

Reasons to dislike Obamacare have abounded from the outset, and on Friday the administration unveiled a new one: In large swaths of the country, the price of insurance sold on the federal health exchange is going up. That will force many of those who bought coverage last year to scramble to find a new policy or fork over as much as 20 percent in higher premiums. How's that "affordable" health care working out for you?

Republicans in Congress � less inclined than some deep thinkers to sneer at "the stupidity of the American people" � unanimously opposed the Affordable Care Act when it was enacted, and were rewarded in the 2010 midterms for their steadfastness. In the ensuing four years, Republicans repeatedly called for replacing Obamacare with alternatives expanding choice, competition, and market reforms � and the voters just rewarded them again.

Of course, even with their new majorities in Congress Republicans will have to contend with President Obama's veto pen. So a bill "repealing every last vestige of Obamacare," as Senator Rand Paul of Kentucky exuberantly proposed on Election Night, isn't in the cards anytime soon. But that doesn't mean there is nothing to be done, particularly since the Supreme Court has agreed to hear a new challenge to the law, one that could potentially cause Obamacare to topple under its own weight.

One way or another, changes in the law are coming. Not all of them have to be bitterly controversial, or provoke cries of Republican overreaching. Here's a suggestion: Allow individuals to buy health insurance from out of state.

In an age when consumers can purchase almost anything from vendors almost anywhere, government policies protecting insurance companies from interstate competition are indefensible. Lawmakers would be laughed out of office, rightly, if they insisted that the only CDs, cellphones, or ceramics their constituents could buy were those manufactured in the state where they lived. All sorts of financial products are routinely acquired without to state borders proving an impenetrable barrier: life insurance, service warranties, stocks and bonds, bank accounts, credit cards. Why should a medical plan be any different?

There is no good reason to deny freedom of choice to Americans when it comes to buying health insurance. Yet licensing rules in virtually every state effectively prevent individual residents from shopping for health plans in any other state. Consequently, there is no national market for health insurance. There are only autonomous state markets, many dominated by near-monopolies that can get away with offering lower quality insurance at ever-higher premiums.

As Michael Cannon of the Cato Institute points out, it isn't only insurance companies that are sheltered from the rigors of competition. Insurance regulators are insulated too. State governments, inveigled by special interests, can burden health insurance policies with more and more mandatory benefits, driving up premiums to cover services that many consumers would never willingly choose.

In Massachusetts, for instance, health insurance policies must cover at least 49 specified treatments and types of providers, among them midwives, infertility treatments, hair prostheses, and chiropractors. But what if all you want is a plain-vanilla health plan akin to those sold by insurers in New Hampshire (only 38 state-required health-care mandates) or, better yet, in Michigan (24) or Idaho (13)? Tough luck. That's what it means when interstate commerce in health insurance is blocked.

Polls show broad public support for the idea � as high as 77 percent in a recent Rasmussen poll. Legislation to overhaul the Affordable Care Act, currently being drafted by Florida Senator Marco Rubio and Wisconsin Representative Paul Ryan, will reportedly include interstate choice. "We want � every American to be able to buy the kind of health insurance they want at a price that they are willing to buy and from any company in America that will sell it to you," Rubio said in a recent radio interview.

Which isn't to say change can only come from above. One can envision a moderate, pro-reform governor championing such market choice at the state level � a just-elected Republican, say, with a deep knowledge of the health insurance industry. How about it, Charlie Baker?  Why not use that new bully pulpit to advocate for legislation freeing Massachusetts residents to buy a health policy from any properly licensed insurance company in America willing to sell it to them?

Why not use that new bully pulpit to advocate for legislation freeing Massachusetts residents to buy a health policy from any properly licensed insurance company in America willing to sell it to them?

It's a fix long overdue. With the distortions imposed first by RomneyCare and then ObamaCare, Massachusetts could use it more than ever. The rest of the country could too.

Comment by clicking here.